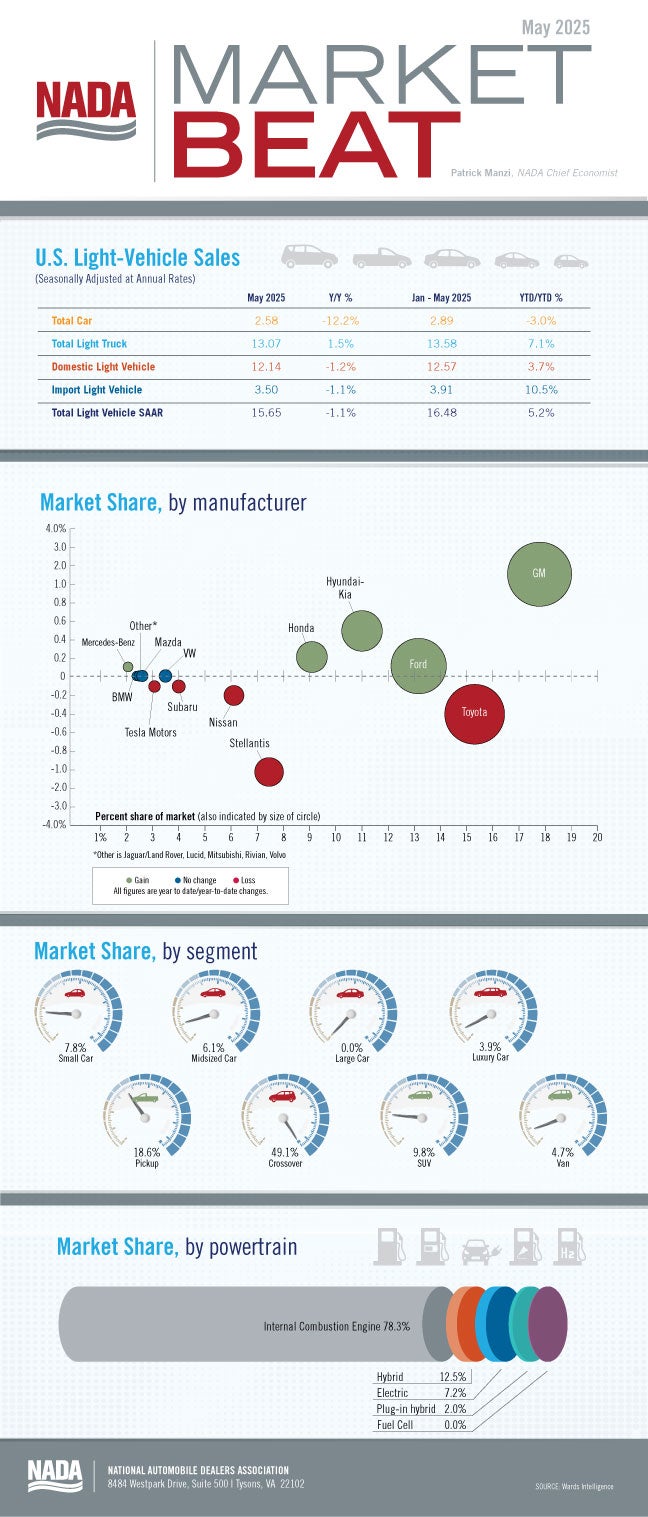

New light-vehicle sales slowed to a 15.7-million-unit SAAR in May 2025, following back-to-back months where the SAAR clocked in above 17 million units. The May sales results fell back in line with pre-tariff expectations. J.D. Power estimates an additional 149,000 vehicles were purchased in March and April 2025, as consumers pulled ahead purchases to avoid tariff-related price impacts. While it is likely there were still some pull-ahead sales in May 2025, it appears the pre-tariff surge in new-vehicle sales has ended. We expect such pull-ahead purchases will result in lower monthly sales later in the year.

New-vehicle production has fallen slightly in the months following the vehicle tariff announcements. Those production declines—coupled with the strong sales pace in March and April 2025—represented the first year-over-year decline in new-vehicle inventory since June 2022. At the start of May 2025, the number of new light-duty vehicles on the ground and in transit to dealer lots was 2.62 million units, a decline of 4.1% year over year. New-vehicle inventory likely will cool even more once final May 2025 data are available. With solid vehicle demand and a tighter supply of new vehicles in May, OEMs have been under less pressure to incentivize sales with discounts. According to J.D. Power, average incentive spending per unit is expected to total $2,563 in May 2025, a decline of $200 compared to April 2025 and down $143 year-over-year.

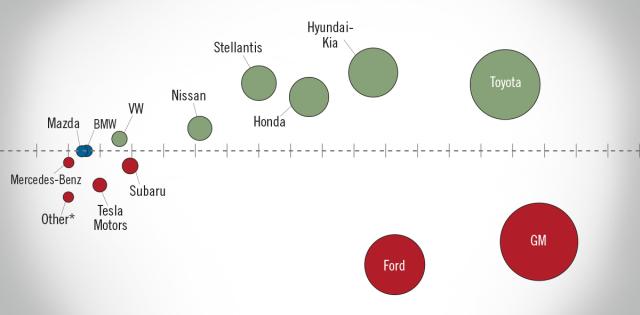

In the coming months, we expect all OEMs to be affected by the tariffs on imported vehicles and parts, although the cost impacts will be much greater for some OEMs than others. So far, each OEM has been taking its own strategy when dealing with the cost increases, but the burden of these increases will be borne by OEMs, dealers and consumers alike. Exactly how much each OEM will be affected remains to be seen as the higher costs work their way through the vehicle-supply chain. Our outlook for new light-vehicle sales in 2025 has been lowered to 15.3 million units.