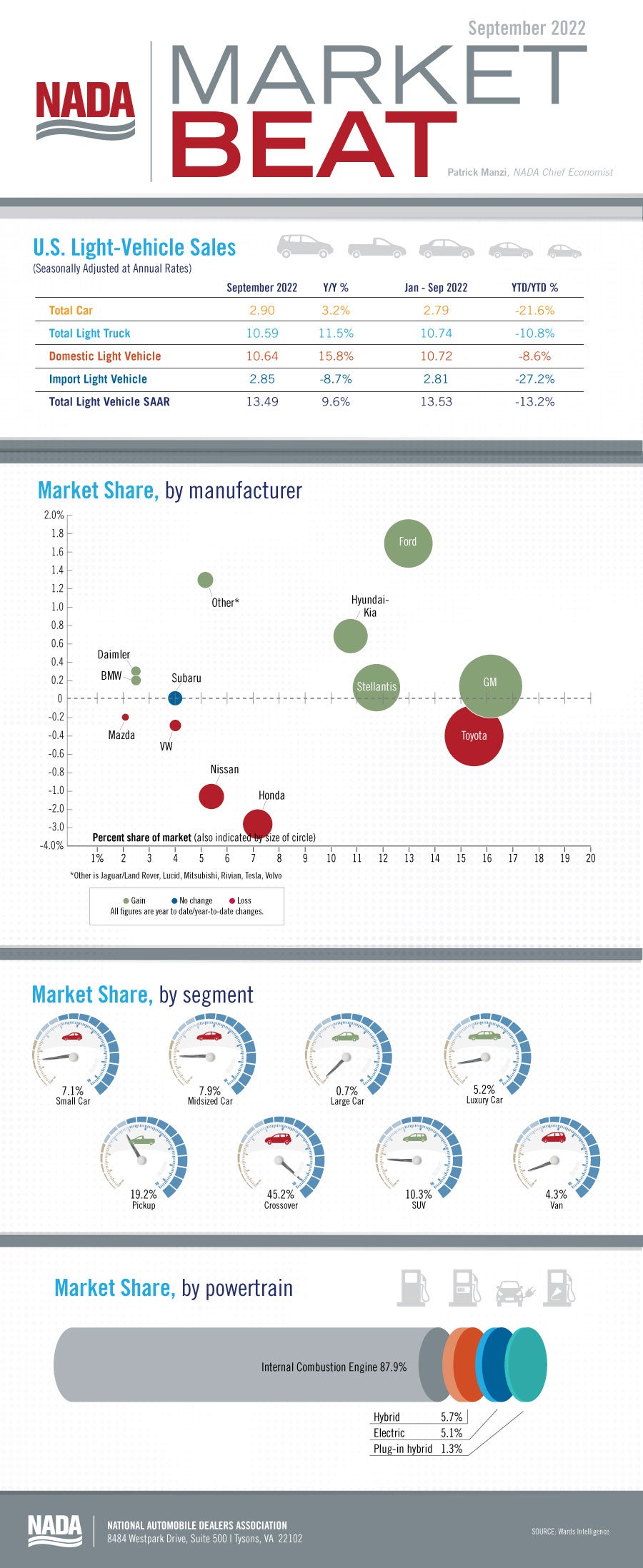

New light-vehicle sales in September 2022 totaled a SAAR of 13.5 million units, up 9.6% from a year ago. New light-vehicle sales in September 2021, the weakest since May 2020, were limited by the lowest inventory level on record for at least 36 years. While not a return to normal by any means, inventory levels at the end of September 2022 should be above the bottom seen a year ago and should be higher than the end of August 2022’s 1.27 million units on the ground and in transit. September 2022’s sales brought the Q3 2022 average SAAR to 13.3 million units, roughly flat compared with Q2. Sales in September continued to be limited by available inventory but were also impacted somewhat by Hurricane Ian. Despite improvements to vehicle availability, some consumers may be stepping back from the current market and its higher-trimmed, higher-priced mix of vehicles.

Transaction prices remained at near-record levels in September. According to J.D. Power the average new-vehicle transaction price is projected to reach $45,622, up 10.3% year over year and the fourth-highest price ever. Although there has been some consumer pullback because of the mix of available vehicles, it hasn’t been enough to dramatically alter the level of OEM incentive spending. Average incentive spending per unit is expected to total $936, down 47.8% year over year and the fifth straight month of sub-$1,000 average incentive spending, says J.D. Power. As the Fed continues to increase the federal funds rate to cool inflation, rates for new- and used-vehicle finance contracts have risen as well. According to J.D. Power, the average interest rate on a new-vehicle finance contract will likely reach 5.71% in September. The month’s average interest rate would represent an increase of 169 basis points from September 2021 and would mark the first month since the pandemic began that the average rate on a new-vehicle finance contract was above its February 2020 average of 5.5%.

For the rest of 2022, we expect that inventory levels will continue to increase slowly but steadily, hopefully providing consumers with more vehicle choices. The Fed will likely push rates even higher at its final two meetings of the year, putting even more upward pressure on consumers’ average monthly payments. New light-vehicle sales should end the year down from 2021’s full- year total, but we still foresee 2022 as being another great year for America’s franchised dealers.

For more stories like this, bookmark www.NADAheadlines.org as a favorite in the browser of your choice and subscribe to our newsletter here: