NADA Market Beat

Produced by NADA's Industry Analysis division, NADA Market Beat is a monthly report on U.S. new light vehicle sales; it replaces the NADA Monthly Sales Recap.

NADA Market Beat: New Light-Vehicle SAAR Hits 15.9 Million Units in April 2026

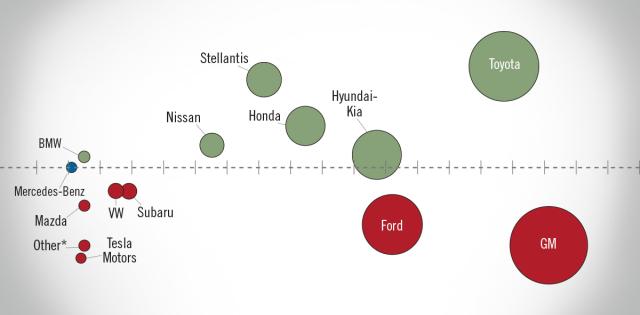

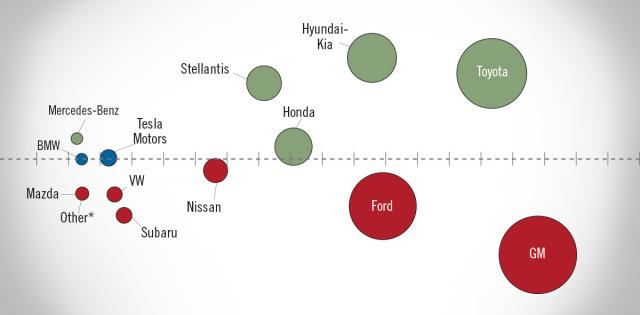

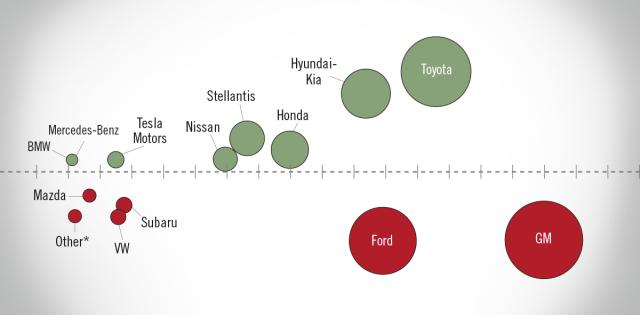

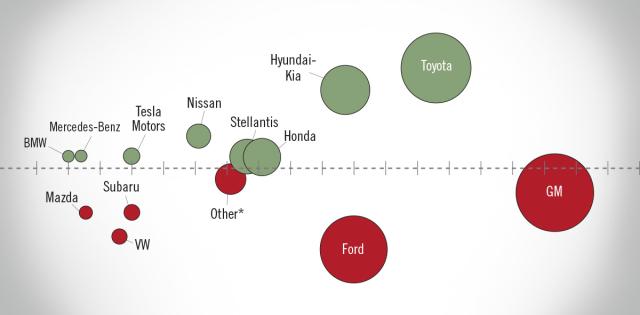

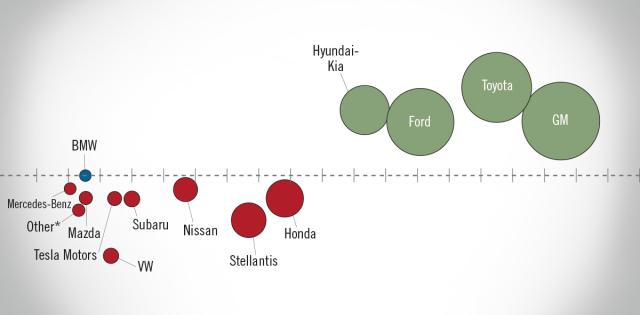

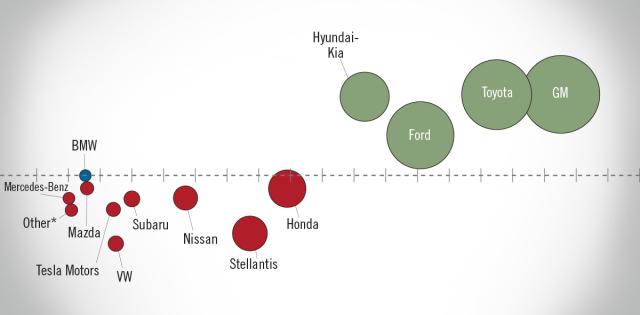

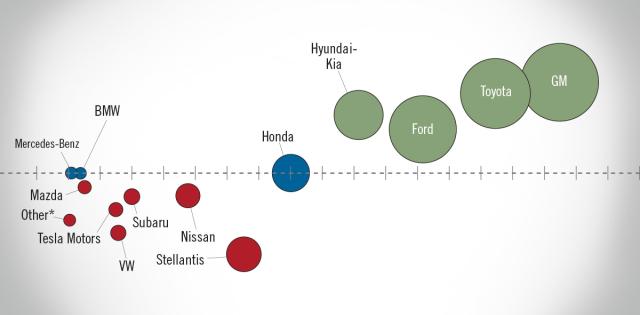

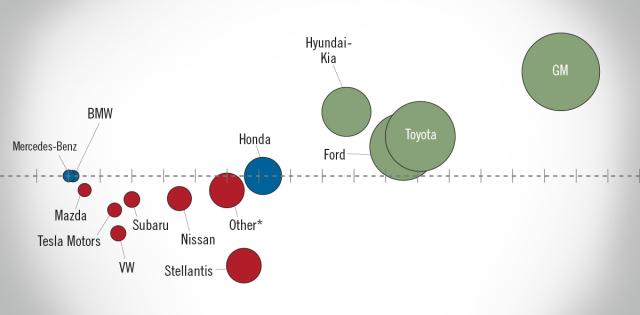

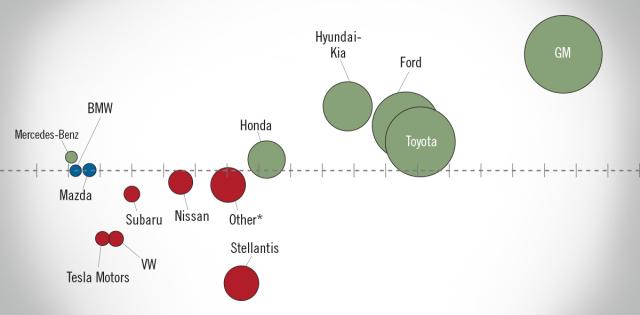

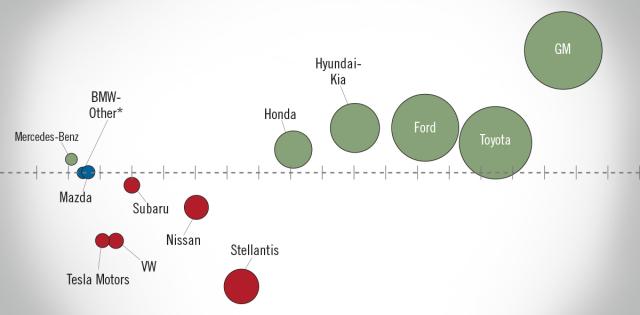

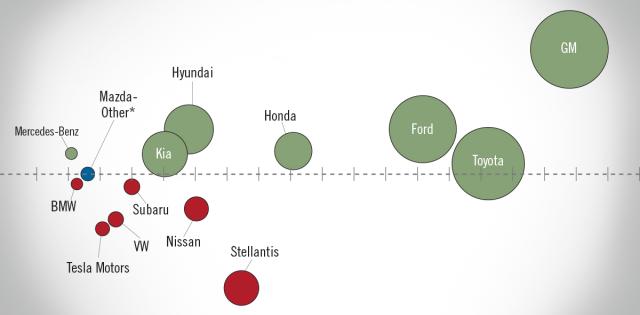

New light-vehicle sales in April 2026 reached a SAAR of 15.9 million units, a decline of 7.1% compared to April 2025 and the eighth straight month of year-over-year declines.

New light-vehicle sales in April 2026 reached a SAAR of 15.9 million units, a decline of 7.1% compared to April 2025 and the eighth straight month of year-over-year declines. April 2025 was the final month before tariffs on imported autos and auto parts went into effect and, as a result, March and April 2025 included significant pull-ahead sales volumes as consumers tried to buy before tariffs took effect. Year-to-date through April, the new light-vehicle SAAR was 15.6 million units, down 6.7% year over year.

Conventional hybrid vehicles were the only powertrain group to post year-over-year gains in April. Hybrid sales year-to-date through April 2026 were up by 9.2%. And hybrids represented 14.5% of all new vehicles sold so far this year, up 2.1 percentage points compared to the same period last year. Battery electric vehicle (BEV) sales continue to post year-over-year declines and were down by 35.5% through the first four months of the year. BEV market share totaled 5.1% through April 2026, a decline of 2.3 percentage points of market share compared to the same period in 2025.

Vehicle affordability continues to limit the pace of new-vehicle sales. High interest rates and monthly payments are limiting the buying pool. JD Power estimates that the average new-vehicle monthly payment will be $812 in April 2026, up 3.1% year over year. According to JD Power, the average interest rate on a new-vehicle finance contract will be at 6.7% in April 2026. Average new-vehicle interest rates have been relatively sticky over the past year ranging between 6% to 7% despite reductions in the Federal Funds Rate last year.

The war in Iran and closure of the Strait of Hormuz continue to disrupt global commodity flows as oil and gas production continues to be disrupted in the region. Most parts of the U.S. are now seeing average gas prices well above $4 per gallon. Omdia notes that OEMs have indicated it will take sustained gas prices of greater than $5 a gallon before we start to see big industry-wide shifts in the vehicle mix.

Archive

The Auto Industry Event of the Year

Orlando | February 17-20, 2027 (Wednesday-Saturday)